How are the energy markets before winter?

Gas supplies in European countries are very comfortable in the first half of winter. Gas imports from Norway and liquefied gas from overseas are running smoothly. Storage facilities were sufficiently filled before winter, and weather forecasts currently indicate a warmer winter.

Only Germany, which has lower than usual volumes in its storage facilities, poses a potential risk to the Czech Republic if the second half of winter is consistently colder than normal. In such a case, stocks in Germany would be completely depleted and the price would rise compared to the reference market in the Netherlands. This would lead to higher gas prices in the Czechia as well.

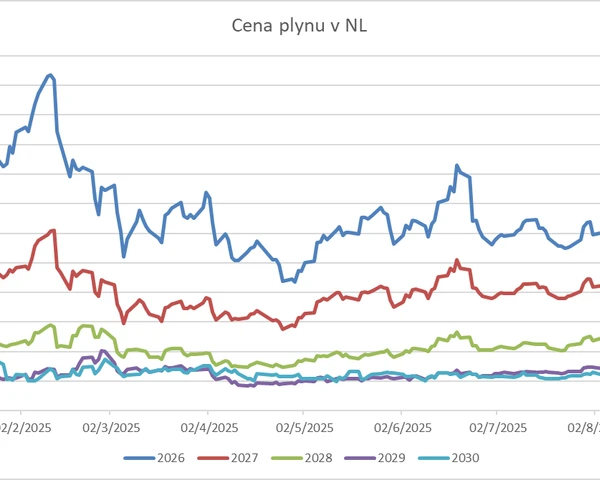

Demand for gas in Asia remains weaker, while supply, especially LNG, is slowly growing. Prices thus continue to fall. As of 2 December, prices for delivery in 2026 are around EUR 28/MWh, which is about EUR 4/MWh less than at the end of the summer. If the warmer weather forecast comes true, we can expect prices to fall further to a level where price-sensitive demand in Asia is activated. We see the first so-called price anchor at around EUR 26–27/MWh.

It is still true that future prices should be lower than current prices. We are gradually moving from a shortage market to a surplus market, with the years 2027–2030 in particular coming under strong supply pressure.

At the same time, preparations are underway to postpone the validity of the ETS 2 system by one year, to 2028. This system will lead to a levelling of market conditions, and emission allowances will apply to virtually all emitters, including households, in the prices of purchased products and services. In the summer of 2026, consultations will also begin on amendments to the ETS 1 system, which defines the rules for the payment of emission allowances for electricity producers and large industrial companies. The discussions will focus in particular on the mechanisms determining the volumes of emission allowances offered in primary auctions.

Given that the price of electricity is significantly influenced by the price of CO₂, pressure to reduce or regulate it can be expected, for example in the form of an increase in the quantity of allowances offered, the introduction of price caps or other measures.

We are also seeing a mass cancellation of hydrogen production projects and a general reduction in support for renewable energy sources. Not only in Germany are concessions being introduced for manufacturing companies, for example in the form of discounts on the price of electricity or by transferring part of the regulated components of the price from end consumers to the state budget. However, these are not systemic solutions, but rather short-term "firefighting" measures that will cost taxpayers dearly in the form of higher public debt. Moreover, these measures undermine the unity of the European market and force other countries to respond in a similar manner.

What does this mean?

Over the next three years, we will see more realistic Green Deal targets being set. It is possible that the ban on combustion engines will be lifted, or that the commitment to carbon neutrality by 2050 will be abandoned and transformed, for example, into a target of 70-80%. We can also expect a change in the approach to reducing emissions, such as a return to nuclear and gas for part of electricity production.

A change in the design of the free electricity market, adjustments or the cancellation of subsidies cannot be ruled out either. Gas prices may easily fall below EUR 20/MWh in the future.

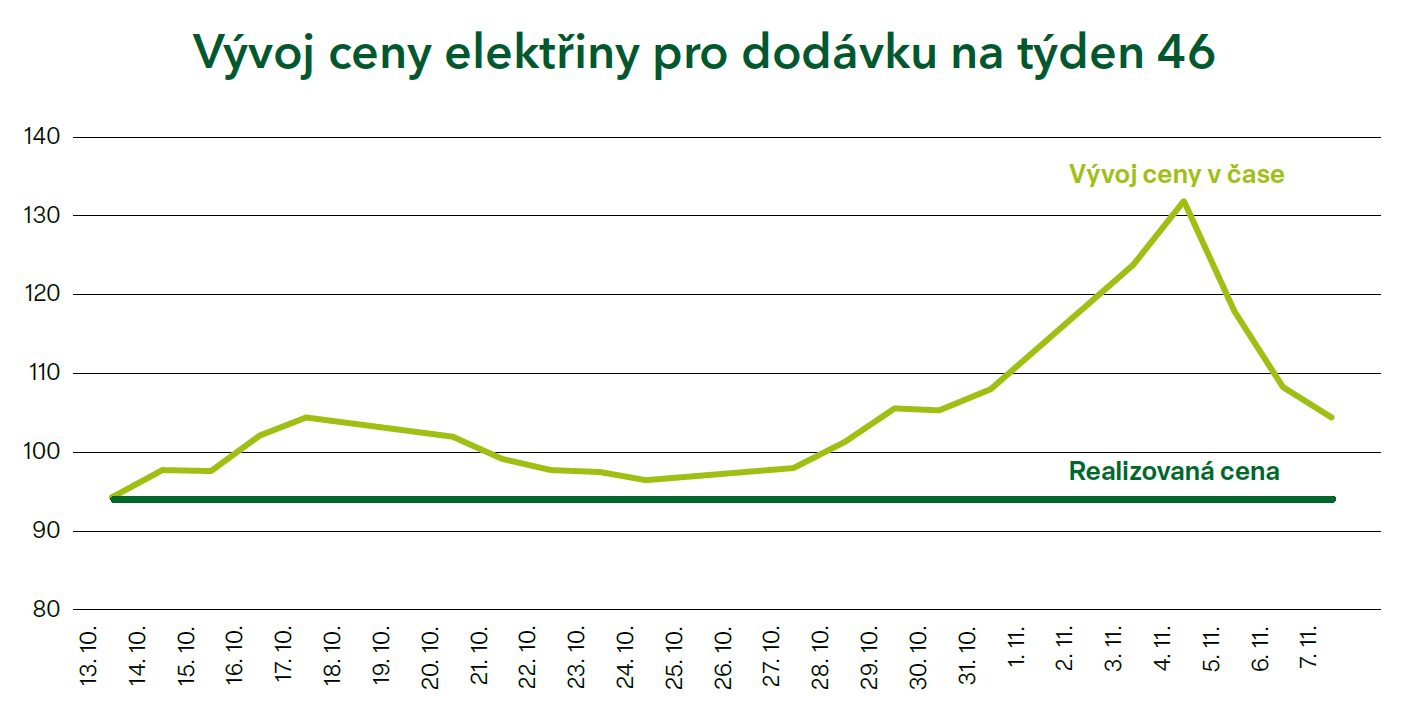

The situation on the electricity market is completely different. In autumn and winter, the main drivers are forecasts and actual wind power generation. This year, forecasts are extremely volatile and show large deviations, leading to significantly fluctuating electricity prices with delivery one day to several weeks in advance.

Gradual revision and more realistic formulation of Green Deal targets

Europe is beginning to realise that the costs of transforming the energy sector and the economy towards carbon neutrality are very high. The impact on industrial competitiveness is negative, and in some sectors even devastating. Politicians are also beginning to realise this, which is reflected in a change of rhetoric in the European Parliament and in national parliaments.

European countries agree on postponing some measures and reassessing the pace of transformation. The environment will be very dynamic and it is necessary to monitor it actively. That is why we are involved in working groups at the Energy Traders Europe association, which are participating in the revision of European market rules and related energy legislation.

The role of oil in the coming years

How are the transformation steps reflected in the oil market? The International Energy Agency's models worked with a "green scenario" according to which there would be a rapid transformation of the economy and global oil demand would peak in 2026–2028. We do not agree with this view in the long term.

Demand for oil is driven primarily by the developing countries of Asia, Africa and South America. From this perspective, Europe is more of a marginal market. We believe that global demand for oil will grow until around 2050. This view is beginning to be confirmed by comments from analytical firms and banks, which are pushing the peak of consumption further into the future. This is positive news for miners.

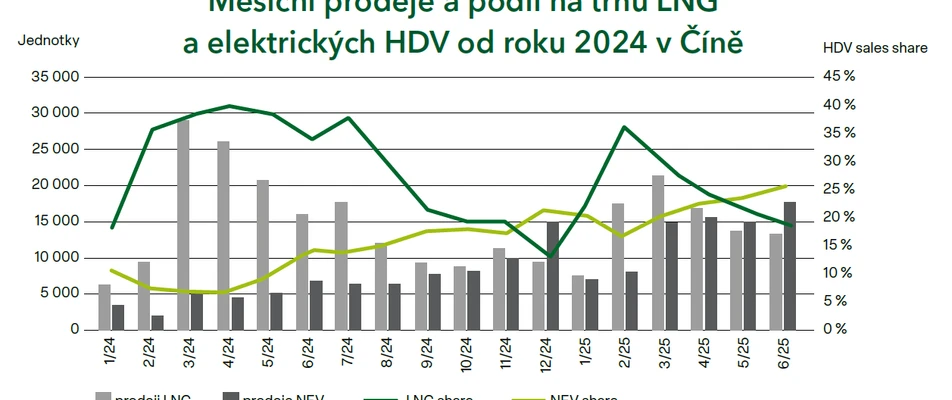

However, the electrification of the economy remains a long-term trend. This can be clearly seen in China, which has not only shifted part of its freight transport from diesel vehicles to liquefied gas-powered vehicles, but has also seen a significant increase in sales of electric trucks in the last year. Further improvements in battery technology and the gradual replacement of oil in transport by electricity can be expected – but only if it is available at a sufficiently low price.

Director of Trading Division

Other articles

Trading 2025: volatility and new opportunities

The year 2025 proved unfavourable for trading activities. Since the new US administration took office, an unpredictable ‘storm’ of tariffs has raged. The markets were unable to cope with this – and we were no exception. There were sharp fluctuations in energy commodity prices simply on the basis of Donald Trump’s comments on Twitter or in reaction to a newspaper headline, even though the latter contained no new information. A very unfortunate period.

How are the energy markets before winter?

Gas supplies in European countries are very comfortable in the first half of winter. Gas imports from Norway and liquefied gas from overseas are running smoothly. Storage facilities were sufficiently filled before winter, and weather forecasts currently indicate a warmer winter.

The unease in the markets continues

This summer, usually a period of holidays and rest, did not show the typical calm on the markets at all. On the contrary. The frequent change in US attitudes has continuously caused chaos and difficult-to-predict price movements.