Market and storage capacity impacts of the UA gas transit closure

At the end of 2024, the five-year contract between Russia's Gazprom and Ukraine's Naftogaz for gas transit to Europe expired. Ukraine had previously announced that it was not interested in extending the contract, so the gas flow was stopped as of 1 January 2025.

What does this mean for the ability of European countries to fill their reservoirs? Will it also have implications for Czech, European or even global gas prices?

Approximately 400 GWh of gas flowed through Ukraine per day, i.e. approximately 146 TWh per year (For comparison: the Czech Republic has a consumption of approximately 75 TWh/year). This is a volume that is already significant not only for Europe but also for the global gas market balance. Why also for the global one? Because Russia is not able to redirect the same volume to other markets. And this means that Europe has to meet its needs mainly with liquefied natural gas (LNG). Thus, demand for LNG will rise, while supply will fall. The market is clearly reacting to the fact that the balance of the gas market in 2025 is worse than it was in 2024, and that the market is significantly more sensitive to weather and supply-side fluctuations.

Europe will therefore have to compete for LNG with other countries such as China, South Korea, Japan, India, Egypt or Brazil. In order to attract ships here, the price of gas in Europe must be higher than in other countries (after taking into account transport costs, of course). Prices will increase until the level at which demand is reduced. This will happen first in the Asian countries. At prices somewhere around EUR 60/MWh we should see the first impacts on consumption. There will be a substitution of coal and oil products for gas in power plants and, in fact, wherever technologically possible. Generating electricity in this inefficient and dirty way will simply be cheaper. There will also be a substitution of LNG in freight transport back to diesel (China).

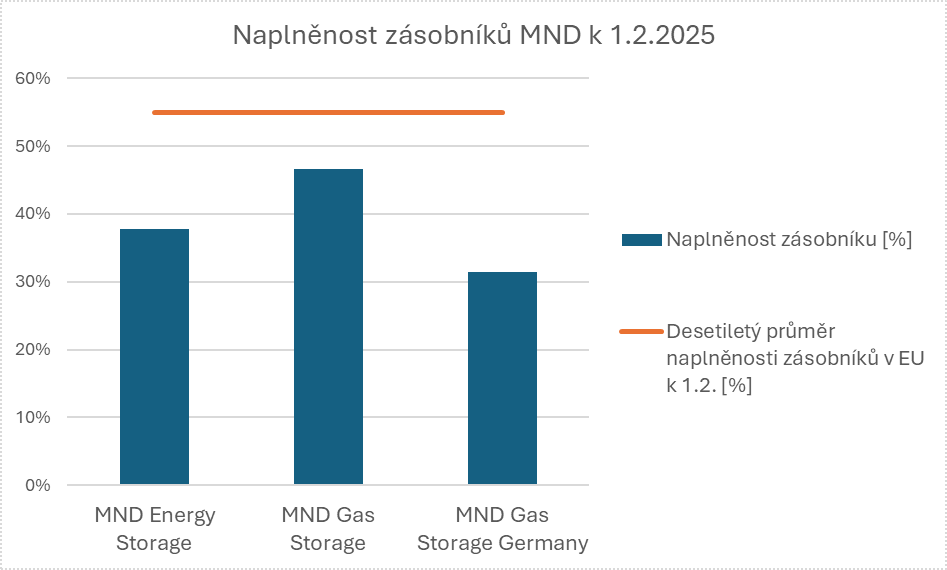

Gas stocks in Europe are falling faster than in 2024 because of the colder winter. The lower the stock levels at the end of March 2025, the more gas demand for injection in the summer and the higher the price can go.

Germany's decision on whether to subsidise storage operators for losses from the sale of storage capacity at a negative price will be very important for pricing. If the subsidy is granted, then prices will rise because the market will know that storage will fill up at any price. However, if the Germans behave rationally, then prices will have rather limited room to rise.

The market is very aware of the European Union's rules for filling storage tanks on 1 November. It is 90%. While there are no penalties for non-compliance, Germany has written the EU limits into its implementing decrees and defined a mechanism that automatically means that the gas system operator THE (Trading Hub Europe) is obliged to ensure fullness according to the rules. If we know that the storage facilities will be 90% full, at least in Germany, and we know that from winter 2025 onwards, the supply of LNG on the global market will increase significantly, then we have an imbalance in the market: an excess of demand in summer and an excess of supply in winter.

In general terms, we see the need to adjust the current legislation, which is still quite strict, on the sale of storage capacity. At the moment, a consultation process is underway to draft a framework for gas storage in the Decree on gas market rules. For example, storage operators agree with the proposal to define a part of storage capacity (specifically 30% is under discussion) that can be sold in an alternative way, i.e. other than strictly by auction. Furthermore, a proposal to reduce the time limit for the auction to 48 hours from the time of publication could help to better respond to the market situation. The value of storage capacity would also be enhanced by relaxing the European and nationally set minimum limits for filling storage capacity during the year.

The year 2025 will be quite opaque and prices will be very sensitive to changes in supply and demand. From 2026, however, there will be a turnaround. Supply will improve significantly and price sensitivity to events will be lower. This will also mean a fall in prices. The market is already trading much lower today (10 February) for 2026, e.g. summer 2025 at EUR 57/MWh, while summer 2026 costs EUR 43/MWh. The market will gradually stabilise and find its equilibrium level in 2026. We are of the opinion that, unless conditions change, prices in 2026 should on average approach the EUR 35-37/MWh price level.

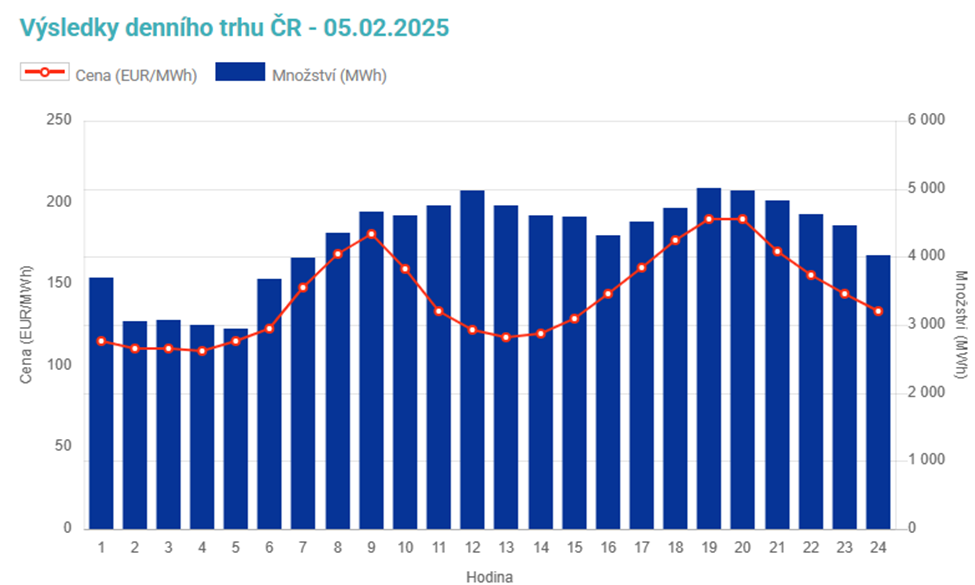

Unfortunately, the deterioration in the global gas balance has also spilled over into electricity prices and emission allowances. How? If the price of gas goes up to a level where it is more profitable to burn coal than gas, then the demand for emission allowances rises and their price increases. And if the price ofCO2 goes up, then that translates into electricity prices. In addition, gas plants are flexible, so they cover what coal plants can't, such as morning and evening peaks (8-10am and 7-9pm). The price of these hours is then of course affected by the price of gas-fired generation. And to make matters worse: the higher the price of electricity, the greater the price fluctuations when the wind blows or the sun shines. As I have noted in previous issues, the price of electricity within a day has a large variance, see the graph of the spot price of electricity for the day of February 5.

Various negotiations are currently taking place at the level of representatives of the European Union, Ukraine, Russia and the United States. At the European level, a relaxation of mandatory storage capacity limits is being discussed. Possible conditions for ending the conflict between Russia and Ukraine are being discussed. All this is reflected in price expectations. For example, the resumption of gas flows through Ukraine would mean a rapid fall in prices and a return to a more normal distribution of prices over time. It would be easier to fill storage tanks. This makes it very difficult to predict prices and price ratios for individual periods. Any report on the subject can move prices quickly in either direction.

Martin Pich

Director of Trading Division

Other articles

Archa III is already helping to preserve cultural heritage in Ukraine

On the premises of the Kyiv-Pechersk Lavra, one of Ukraine’s most significant spiritual and cultural centres, representatives of the Ministry of National Defence, the Karel Komárek Family Foundation (KKFF) and the National Museum handed over the Archa III mobile conservation unit to the Ukrainian side. The device is capable of producing 3D scans of objects of various sizes in the field, ranging from small artefacts to historical items.

Both the state and customers will benefit from battery storage, says Martin Pich

Battery storage is rapidly becoming a key component of the modern energy sector. It is not just about the technology, but also a new way of generating revenue from flexibility whilst stabilising the grid. Martin Pich, Director of the Trading Division at MND, explains exactly how this business works in practice.

The conflict in Iran and its impact on energy markets and prices

The market entered 2026 on a very optimistic note. Individual liquefied natural gas export projects were proceeding according to plan, and the forward market was pricing in a very healthy supply of gas, meaning prices remained low. The same was true for electricity and oil. But then came the turn of February and March, and everything suddenly changed.