Investment opportunity: balancing the energy grid

MNDs are looking at different market segments where it would be worthwhile to invest or at least be commercially active. One of the areas that caught our attention is the market for ancillary services and the volatility of electricity prices on the so-called spot market, where the price of electricity for the following day is determined. In cooperation with the Energy & Production Division, we are working on using our own gas for electricity generation (G2P Borkovany) and on investing in battery storage.

What are support services?

The transmission system operator, the state company CEPS (Czech Electricity Transmission System), is responsible for maintaining the stability of the grid. It models what the balance of electricity in the country will look like in the next fifteen minutes, the next hour, by the end of the day, the next day, month, quarter, year, etc. and plays an important role in planning the state energy concept. It is a never-ending, ever-recurring process. In order to make the calculations, the CEPS must have the necessary data on generation and consumption, temperatures, light, wind strength and cross-border power exchange.

CEPS does not own any power plants, but buys services from electricity producers in tenders. This means that it reserves their generation capacity, which it can "move" online, i.e. reduce or increase production to keep the grid in balance. For this service, CEPS pays a two-component price: a price for the capacity reservation in EUR/MW and a price per MWh produced. If a trader, say an MND, is out of balance, i.e. e.g. it has purchased less energy than it has consumed, then the market operator will charge it for the cost of covering this variation. The costs are based on the services purchased by the CPP.

The main causes of grid imbalances are the constantly changing consumption of end-users and, in particular, fluctuations in renewable generation. In the case of the Czech Republic, this is mainly photovoltaic power plants. The larger the share of solar generation in total generation, the greater the fluctuations and the greater the need for CEPS to purchase larger volumes of services. This is compounded by the fact that stable coal sources will cease to be used in the coming years. And this is precisely the opportunity for new flexible resources such as battery storage and flexible gas resources.

Let's take a look together at what this opportunity looks like

European markets are interconnected and we need to keep an eye on the balance of Western Europe in particular. Across Europe, coal-fired power plants will be shut down and the share of renewables in power generation will continue to grow strongly. We are already seeing how heavily oversupplied the market is in the 'solar' hours, while other hours have to be covered by conventional sources. There is an imbalance between supply and demand and grid operators are struggling with grid stability.

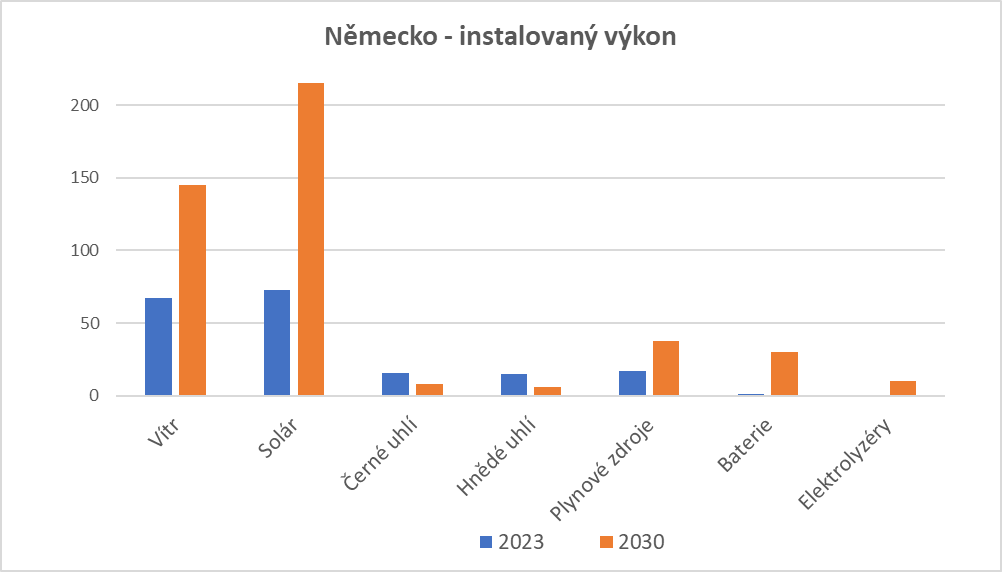

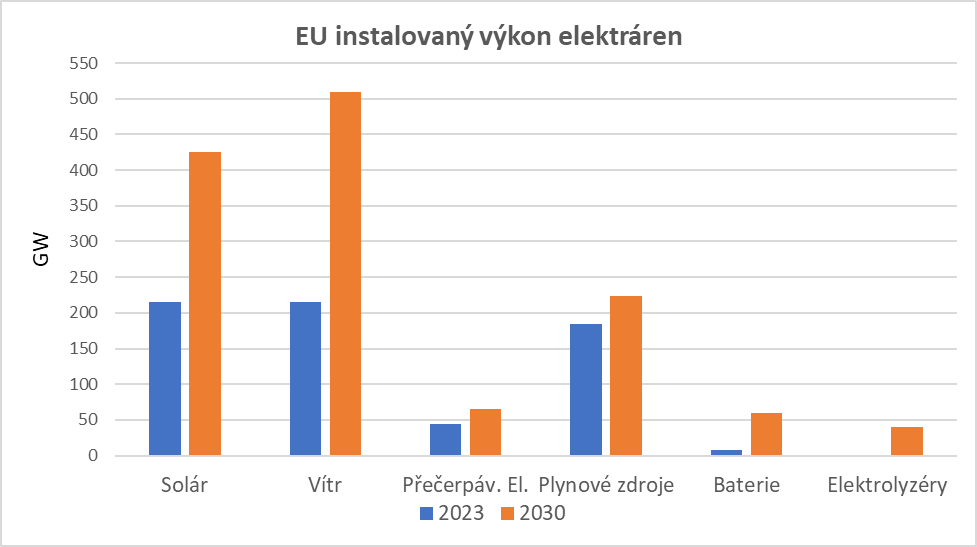

Charts 1 and 2 illustrate that planned construction of batteries and new flexible resources is lagging behind the growth of renewables.

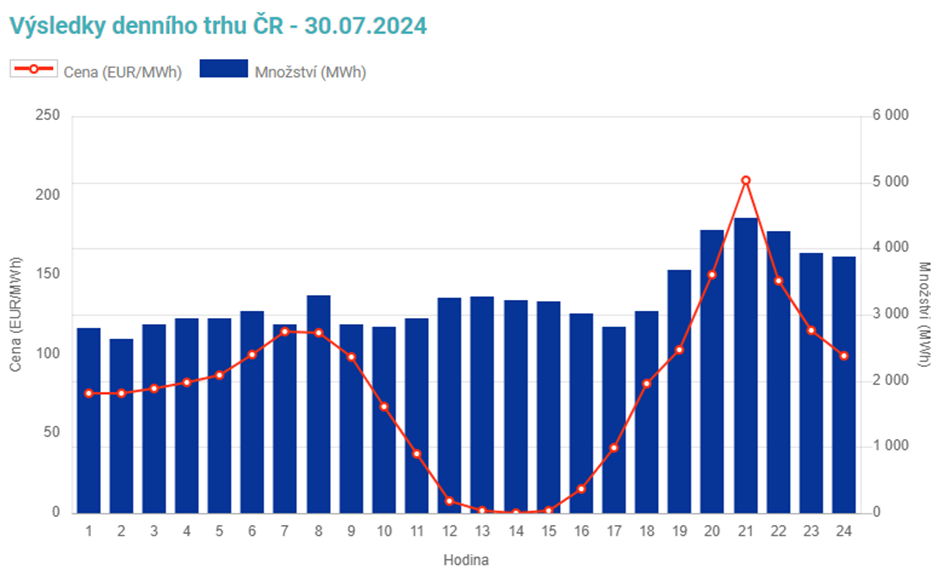

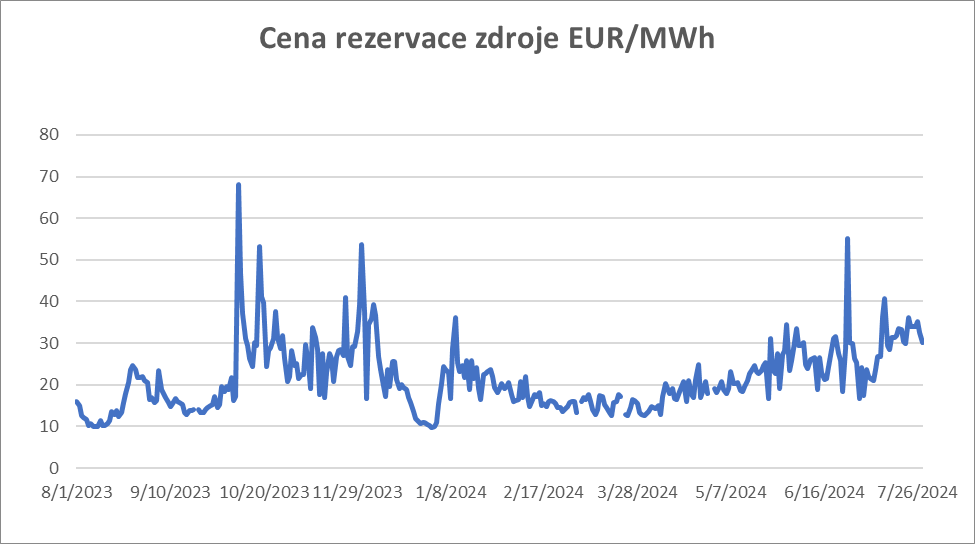

Chart 3 then shows electricity prices in the CZ, with a good indication of the large price differences already emerging. This is ideal for batteries in particular, which are charged at low prices and discharged back to the grid at a significantly higher price.

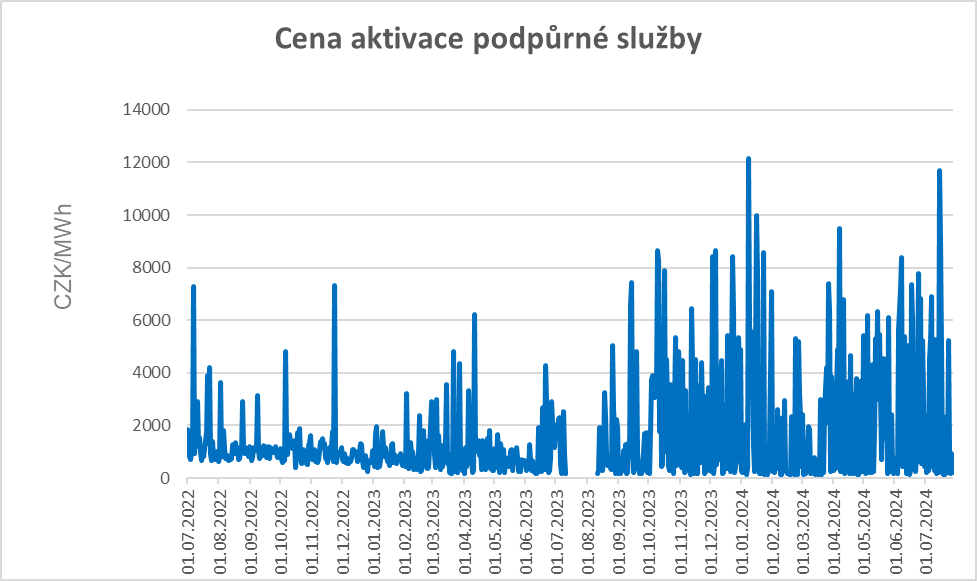

The battery and gas resources can also be used to provide support services for the CEPS. The price increases can be seen in Figures 4 and 5. The activation price is the payment received by the service provider for each MWh generated.

The reservation price is the payment that the service provider receives for making its resource available to CEPS and not otherwise using it. The provider will receive the payment even if the resource is not used by CEPS.

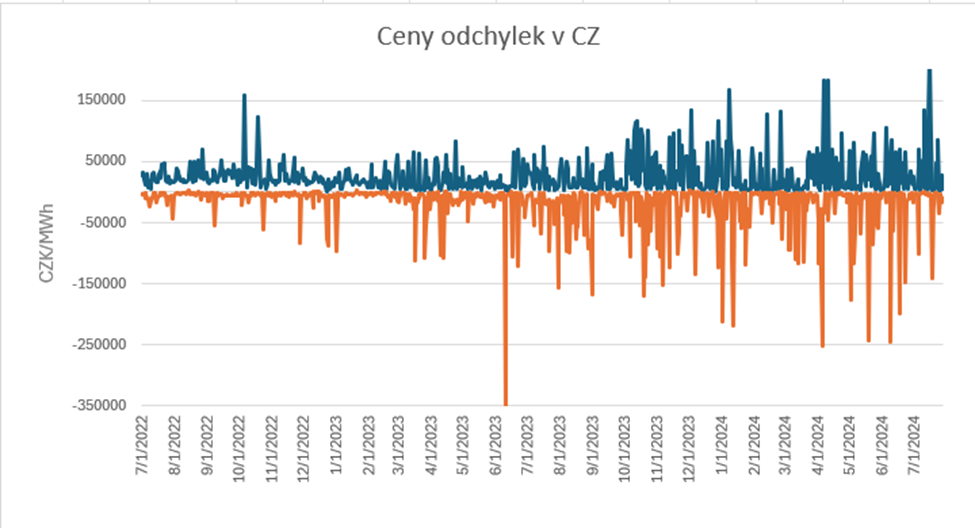

Another great opportunity for flexible resources is the deviation market. We have developed forecasting models that predict the balance of the system. This will allow us to seamlessly decide whether to discharge the battery on schedule or shift the discharge over time based on where more value is being added. In the same way, we can run a gas source according to the same principle. We can also use the reverse motion, i.e. charge the battery or stop generating when there is too much electricity in the system. The deviation prices in CZ are shown in Figure 6.

The transformation of the power sector is a very fast-paced process and brings a lot of turbulence to the whole process of electricity production/consumption and management of the power system. Many new technologies and proposals are emerging on how the sector should develop further. It is virtually impossible to define which technologies will take off in the long term. We are therefore only focusing on the next ten years or so, when it is likely that the price of electricity on the spot market will fluctuate significantly and the need to stabilise the grid will be great. And this is the playground on which we want to be active.

Director of Trading Division

Other articles

Continuing Gas To Power projects

We are currently working intensively on two new energy projects: we are building both the Hrušky 5 ancillary services facility and the SNaPS Ždánice combined heat and power plant.

How are the energy markets before winter?

Gas supplies in European countries are very comfortable in the first half of winter. Gas imports from Norway and liquefied gas from overseas are running smoothly. Storage facilities were sufficiently filled before winter, and weather forecasts currently indicate a warmer winter.

The unease in the markets continues

This summer, usually a period of holidays and rest, did not show the typical calm on the markets at all. On the contrary. The frequent change in US attitudes has continuously caused chaos and difficult-to-predict price movements.