Uncertainty in markets persists

In the last issue, I discussed the impact of the end of gas transit through Ukraine and concluded by stating that 2025 is a tight year in terms of balance. And how have markets developed since then?

Much has changed. The unconventional negotiating style of the American representation has caused chaos in all markets. The stock and commodity markets have experienced and are experiencing major movements. The unleashing of the tariff war has already brought about a gradual cooling of the economies. This has been most pronounced in China's economic activity (container shipping declines, layoffs, production cuts). Naturally, this is associated with a fall in electricity and gas consumption, which has a major impact on global balances. Another important factor then was the comments by the European Union and German politicians that support/subsidies to bunker operators are unlikely to be provided this year. These comments then caused a change in behaviour by the big financial players who bet against the German legislation and the pipeline operators who have an obligation to push gas when it is not profitable for the market. They therefore started to sell their bought positions and sent the price down (see Chart 1). Later, the effects of the tariff war were added. Chinese LNG imports fell and are below last year's levels.

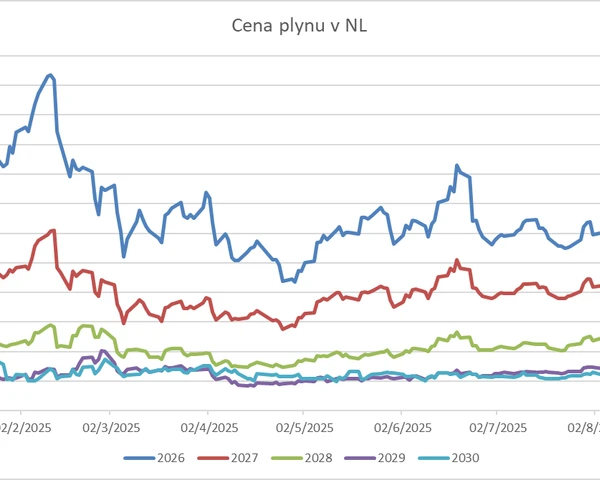

Chart 1. Gas price development for delivery in Q03 2025

The suspension of the extremely high tariffs has already had its first effects. Shipping orders are picking up, which will translate into an increase in production in China and, later on, an increase in consumption of primary raw materials. In addition, we are entering summer, which always brings the risk of increased consumption due to the use of air conditioning. Prices can therefore be expected to rebound and rise slightly during the summer. If EU storage is at least 85-90% full, then prices for 2026 will be rather under pressure as LNG supply, especially from the US and Canada, gradually increases between the end of Q3 2025 and the beginning of Q01 2026. Further projects are due to come on stream during 2026.

Discussions about the possible commissioning of Nord Stream II or a transit via the UA have come up from time to time, but it is unrealistic to assume that we will see any gas flows this year. The EU is working towards a complete cut-off of Europe from Russian gas by 2027 and is preparing for a "ban" on new Russian gas contracts to Europe via other routes (Turkstream, LNG). From 2026, gas from Russia will not be needed. LNG supply is growing rapidly and prices will fall further from 2026. E.g. the delivery price for 2028 is 24% lower than for 2026.

Emission allowance prices have been rising since April, and rising significantly. This was partly due to the need to generate electricity from conventional sources, as there has been long term sub-normal generation from wind power. In addition, there has been discussion about merging the European Union and UK emissions allowance schemes. Financial players were again jumping into position. We already know the final number of allowances in the system for 2025-2026. The gradual removal of allowances from the system naturally puts pressure on the price and financial players always want to be one step ahead.CO2 prices in the timeframe up to 2027 should reach a level of 90-100 €/MWh (unless there is a change in the rules)

Chart 2: Evolution of emissions allowance prices

Electricity prices have followed the development of gas and emission allowance prices, see Chart 3.

Chart 3: Electricity price development for 2026

Oil had a very similar price path. It first fell to USD 58 per barrel when the US announced across-the-board tariffs. Today we are somewhere around USD 63 to 66 per barrel. Demand growth has been slowed while OPEC+ is gradually increasing production as planned. We are seeing a different development in the US, where prices have already gotten too low and investment in new drilling is rapidly declining. We have even seen the first production cutbacks. It could be said that the peak in US production this year is already behind us. These forces are now fighting. We are seeing a wider price range of USD 60 to USD 70. Unless the tariff frenzy can be calmed, prices will fall below USD 60 as individual countries slowly slip into recession. Otherwise, we should see a slow climb to USD 70. If economies show solid growth, we should swing back above USD 70.

Still, this year is anything but easy to predict. The economic environment and confidence between the US and the rest of the world is severely strained. Predicting the actions of the current US representative is, shall we say, "difficult".

Director of Trading Division

Other articles

Trading 2025: volatility and new opportunities

The year 2025 proved unfavourable for trading activities. Since the new US administration took office, an unpredictable ‘storm’ of tariffs has raged. The markets were unable to cope with this – and we were no exception. There were sharp fluctuations in energy commodity prices simply on the basis of Donald Trump’s comments on Twitter or in reaction to a newspaper headline, even though the latter contained no new information. A very unfortunate period.

How are the energy markets before winter?

Gas supplies in European countries are very comfortable in the first half of winter. Gas imports from Norway and liquefied gas from overseas are running smoothly. Storage facilities were sufficiently filled before winter, and weather forecasts currently indicate a warmer winter.

The unease in the markets continues

This summer, usually a period of holidays and rest, did not show the typical calm on the markets at all. On the contrary. The frequent change in US attitudes has continuously caused chaos and difficult-to-predict price movements.