The unease in the markets continues

This summer, usually a period of holidays and rest, did not show the typical calm on the markets at all. On the contrary. The frequent change in US attitudes has continuously caused chaos and difficult-to-predict price movements.

The economic downturn in China in particular, coupled with more gas being produced there than expected, helped keep the gas market in a slight surplus. This has allowed Europe to be well supplied and to pump quickly into storage. As of September 6, 2025, storage in the Czech Republic is 88.8 percent full, and in Western Europe it is 79.2 percent full. All countries will reach the minimum fill rate. In addition, we expect a warmer September and, at worst, normal temperatures for October, and so downward pressure on gas prices can be expected.

But there is one big but: sanctions on Russian gas and oil, which have been intensively discussed between the European Union and the United States in recent days. The announcement of new sanctions from the EU should come in the week of September 8. This may send prices back up again. To what extent? We cannot say. It will depend on the details of the sanctions. We'll have to wait and see. But if it doesn't involve gas, then the markets will ease slightly.

In the longer term, there will still be a surplus of gas and gas prices will continue to fall. The market is aware of the LNG capacity increases and is reflecting this in forward prices.

Similarly, electricity prices are also falling.

However, global gas balance calculations show that prices could fall below the magic EUR 20/MWh level sometime between 2028 and 2031. It will depend a lot on how much consumption changes when the price gets back to really low levels...

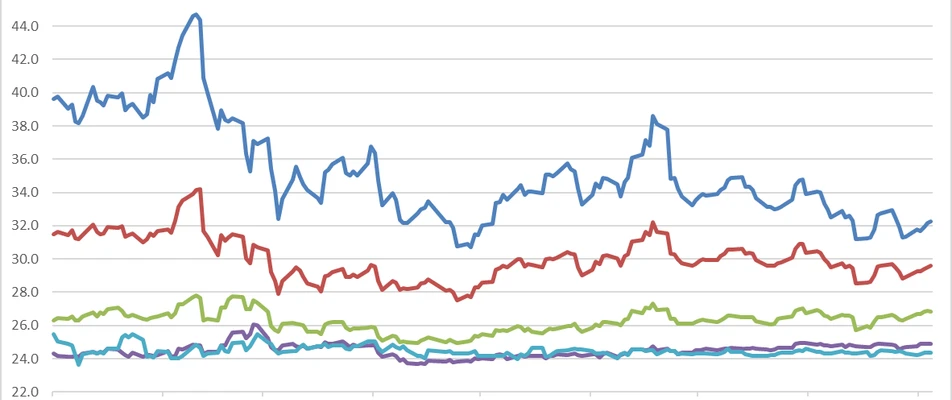

We have seen a very interesting development in the emission allowance market. The summer's very high temperatures in France have caused nuclear power plants to shut down due to high water temperatures in the rivers. EDF has started buying up emission allowances as a hedge against possible price hikes in electricity prices. They are doing this again today as trade unions in France have announced nationwide strikes. US funds responded and started driving the price up further. Speculative 'long' positions, i.e. volumes bought, have increased greatly. They are at unhealthy levels. It is difficult to predict when profit-taking, and therefore selling, will occur and the price will subsequently fall. However, we expect a downward price correction once the situation in France calms down. Physical demand for emission allowances tends to be weaker as gas prices are at levels where it pays to replace coal-fired sources with gas, and with that the need to buyCO2 decreases. However, the projected price decline is very likely to be short-lived. In winter, the price could move back up into the region of over EUR 80/MWh.

The oil market, on the other hand, is relatively calm in its trend. OPEC+ countries are regularly increasing production, thus keeping the market relatively stable in the price range of USD 63-68 per barrel. We are now entering the winter period, which is characterised by cyclically lower demand and prices usually trend slightly downwards. But even here, potential sanctions will skew the oil price upwards.

Commodity markets remain very sensitive to statements by major global political leaders and are therefore difficult to predict. We are living in a period when the wars in Ukraine and Israel are at a very tense stage, tensions between the US and China are rising, and there is the new prospect of a military operation in Venezuela. The situation in Iran, its allied countries and militant groups is still smouldering. The US trade war with the whole world is still changing dynamically. We would like to see a calming down on all fronts and a return to a more normal market.

Director of Trading Division

Other articles

Both the state and customers will benefit from battery storage, says Martin Pich

Battery storage is rapidly becoming a key component of the modern energy sector. It is not just about the technology, but also a new way of generating revenue from flexibility whilst stabilising the grid. Martin Pich, Director of the Trading Division at MND, explains exactly how this business works in practice.

The conflict in Iran and its impact on energy markets and prices

The market entered 2026 on a very optimistic note. Individual liquefied natural gas export projects were proceeding according to plan, and the forward market was pricing in a very healthy supply of gas, meaning prices remained low. The same was true for electricity and oil. But then came the turn of February and March, and everything suddenly changed.